DIC PORTFOLIO

SPANISH NEWS

Naturgy and Sonatrach negotiate a major energy alliance

After months of diplomatic tension, Naturgy and Sonatrach are taking steps towards a comprehensive agreement that would include gas, renewables, and a joint review of prices. Algeria, key to Spanish supply, seeks to strengthen stability and diversify alliances in the midst of the energy transition. For Naturgy, it would be a strategic move that would ensure supply and price visibility for the coming years.

ACS finalizes a €23 billion agreement with BlackRock for a data center

ACS has signed a strategic agreement with BlackRock (through GIP) to create a global data center platform valued at €23 billion. The deal includes a 50% stake in ACS Digital & Energy and an initial joint venture of €2 billion. The plan integrates assets in Europe, the US, and Australia and is looking at more than 11 GW in international projects. With this alliance, ACS is monetizing part of its digital business, reducing debt, and strengthening its presence in the growing cloud and AI infrastructure market. It also confirms the group’s strategy of diversifying beyond traditional construction.

ACS, Ferrovial, and FCC aim for €100 billion from European military plan

The European Union is preparing a mega-program of infrastructure for military mobility, with investments in roads, ports, and logistics. Large Spanish construction companies are well positioned to capture part of the budget. The plan responds to the need to

strengthen common defense and adapt infrastructure to the new geopolitical context. If it materializes, it would be a significant boost for the sector.

Airbus and Indra win defense contracts worth €5.5 billion

The Spanish government has awarded major military contracts focused on helicopters, vehicles, and capacity modernization. Airbus Helicopters and Indra are the main beneficiaries, strengthening their long-term portfolios. The news confirms the acceleration of European military spending in the new geopolitical cycle. For investors, defense remains one of the sectors with the best revenue visibility.

Neinor raises its takeover bid for Aedas to €24 per share

Neinor Homes has increased its offer to acquire Aedas Homes by 12.5%, seeking to convince minority shareholders and close the integration before the end of the year. The transaction would further consolidate the Spanish property development sector and create a larger and more efficient player. The price increase confirms that residential demand remains strong, especially for new construction.

Inditex overtakes LVMH to become the world leader in profits

Driven by its agile distribution models and inventory control, Inditex has managed to surpass LVMH in profits. The Galician company benefits from more stable consumption than luxury goods, which are showing signs of slowing down in some markets. The milestone reinforces its position as a global benchmark in retail. For investors, it sends a clear message: efficiency and adaptation are worth more than size.

Repsol considers mega upstream merger with APA to go public on Wall Street

Repsol is considering merging its exploration and production business with APA Corporation to create a new company that will be listed on the New York Stock Exchange, retaining at least 51% control. The operation would give greater visibility and access to capital to a very investment-intensive business. Repsol’s upstream division (571,000 barrels/day) was valued at $19 billion in 2022 and would fit well with APA’s assets, especially in US shale. The market sees potential operational synergies, but doubts remain about integration, oil volatility, and regulatory risk. The move fits with Repsol’s strategy of leveraging assets through listed structures.

Spanish banks will extend profit growth by another 4% through 2026

With record profits of €25.447 billion (+7.6%), Spanish banks closed the first nine months of the year, supported by higher credit volumes, solid commissions, and still-contained deposit costs. Although the tax on the sector and more stable rates are moderating the pace, the consensus forecast is for further growth of 4% in 2026, with EPS at historic highs. Bankinter would lead the way, followed by BBVA, Santander, Sabadell, and CaixaBank, while Unicaja would be the only one to see declines. Overall, the sector maintains stable margins and provisions, reinforcing its role as one of the drivers of the IBEX.

Grifols harmonizes €1.3 billion in bonds and strengthens its financial profile

Grifols has managed to get the majority of bondholders to agree to modify a €1.3 billion bond to align it with another issue maturing in 2030, removing limits that complicated its refinancing. Changes to clauses relating to subsidiaries, assets, and permitted debt improve its financial flexibility and facilitate the renewal of €740 million in 2026. The consent payment expedited the agreement, which the market interprets as a further step in the normalization of credit risk and the deleveraging of the company.

Sabadell falls despite posting record profits

Through September, Banco Sabadell posted record profits of €1.39 billion (+7.3%). Even so, the stock fell 8.46% as the market expected more. Net interest income was below forecasts and quarterly profits were around 6.5% lower than expected, which generated a negative reaction. In addition, the normalization of interest rates is beginning to put pressure on revenues, and the bank faces a more competitive environment following BBVA’s failed takeover bid. In short, the results were good, but insufficient to sustain the previous rally in the share price.

Apollo Sports Capital buys 55% of Atlético de Madrid

Apollo has acquired approximately 55% of Atlético Madrid in a deal that values the club at €2.5 billion, one of the largest transactions in the history of European soccer. The investment is in line with the fund’s strategy of investing in alternative assets with stable cash flows, such as sports franchises and audiovisual rights. The US fund sees strong growth potential in brand internationalization, digital monetization, and increased revenue from streaming, sponsorships, and stadium operations. The deal confirms the transformation of clubs into global entertainment platforms that are attractive to institutional investors.

EUROPEAN NEWS

Brussels considers total ban on Huawei in European networks

The European Union is considering completely removing Huawei equipment from telecommunications networks, a measure with a significant economic and operational impact on telecommunications companies. The proposal responds to concerns about technological security and dependence on Chinese suppliers. In Spain, replacing the equipment would cost around €4 billion and could strain diplomatic relations with China. If successful, it would be one of the biggest regulatory moves in the Union’s digital infrastructure.

IAG, Lufthansa, and Air France-KLM vie for TAP

Portugal has begun privatizing 44.9% of TAP, sparking intense competition between IAG, Lufthansa, and Air France-KLM. The main attraction is strategic access to the Brazilian market, one of the most profitable and with the greatest growth potential in long-haul flights. The operation could reshape the balance of power in European aviation, changing routes, hubs, and alliances. It would also strengthen the buyer’s position in a sector that continues to consolidate. The Portuguese government’s decision will be key in determining the new European aviation map in the years to come.

The ECB calls for politics not to interfere in bank mergers

Frank Elderson, member of the ECB’s Executive Board, warned that bank mergers should be assessed on technical criteria and without political pressure. He pointed out that European banks are sound and profitable, but need to strengthen their resilience to cope with digitalization, climate change, and geopolitical instability.

He defended the full implementation of Basel III and recalled that mergers, especially cross-border ones, can create more competitive entities. To this end, he called for accelerating the Banking Union and removing barriers that prevent the emergence of truly pan-European banks.

European investment in AI is six times lower than in the US

In 2023, Europe invested only €11 billion in AI, far behind the US’s €67 billion, reflecting a growing innovation gap with the major powers. The continent remains focused on traditional sectors and spends 35% less on R&D, while the US and China are investing heavily in strategic technologies. Among the causes are the fragmentation of the European market, dependence on bank financing, and the lower efficiency of public R&D. Experts suggest promoting pan-European mergers, advancing fiscal integration, and developing a true European capital market to reverse this competitive disadvantage.

INTERNATIONAL NEWS

Warning from fund managers: without a Fed rate cut in December, further declines could be on the way

Managers consulted by BofA warn that the rally of recent weeks could run out of steam if the Fed does not cut rates in December. Still-high inflation and stronger-than-expected macro data have dampened market expectations, causing more volatility and rotation away from technology stocks. Many funds fear that keeping rates at restrictive levels will slow credit and investment in 2025. The message is clear: a monetary policy shift is not yet assured, and that increases the risk of further corrections.

Alerts grow over a possible AI bubble and excessive corporate investment

The pace of investment in data centers, chips, and AI hardware has accelerated so much that some managers fear that overcapacity is beginning to form that will be difficult to make profitable. Big tech companies have announced record CAPEX plans, financed in part by debt, for infrastructure whose return is still uncertain. Following NVIDIA’s latest results, which exceeded expectations but showed signs of high inventories and doubts about the sustainability of demand, the market has intensified sales in semiconductors and cloud-related companies. The recent declines reflect profit-taking after a very prolonged rally and fears that the market has discounted too much growth too quickly. Although the structural trend in AI remains intact, there is a growing sense that there could be excessive enthusiasm in the short term.

The longest shutdown in US history comes to an end

After 43 days of administrative paralysis, the United States has ended the longest federal shutdown in its recent history. The reopening unblocks delayed payments, reduces political uncertainty, and allows for the resumption of key data releases such as employment, inflation, and preliminary quarterly GDP estimates. The shutdown had a real economic impact, with lost growth and a “statistical blackout” that made it difficult to assess the health of the economy. The normalization of data will be crucial for the Fed to gauge its next monetary policy moves.

Significant correction in the AI-related technology sector

The technology sector linked to artificial intelligence experienced a week of selling pressure, with notable declines in chip manufacturers such as Intel (-8.69%), TSMC (-2.72%), and Nvidia (-2.63%), while AMD (+1.63%) was the exception thanks to optimism about its new accelerators. The adjustment was even more intense in the AI server segment, where Super Micro Computer (-11.94%) and Dell (-10.58%) led the declines after several months of strong gains.

The movement also affected the big players in the cloud and corporate AI: Amazon (-5.49%), Alphabet (-2.85%) and Palantir (-5.48%), although it did not affect Microsoft (+2.2%) in the same way. The week saw a tactical rotation in the market following the sector’s sharp rally, with profit-taking and greater selectivity amid fears that the Fed will keep rates high for longer. Despite this correction, AI remains the main structural driver of growth in technology, and analysts see it as more of a technical pause than a change in trend.

Michael Burry closes Scion Asset Management

Known for anticipating the 2008 subprime crisis, Michael Burry has decided to close his fund and stop managing external capital. The decision comes after months of reducing exposure to large technology companies and warning about excessive valuations in companies linked to artificial intelligence. Although he has not detailed his next move, his departure from the professional market reinforces the perception that some leading investors see signs of euphoria in the sector. His contrary position adds context to the debate about possible excesses in the race for AI.

LEARNING POINT

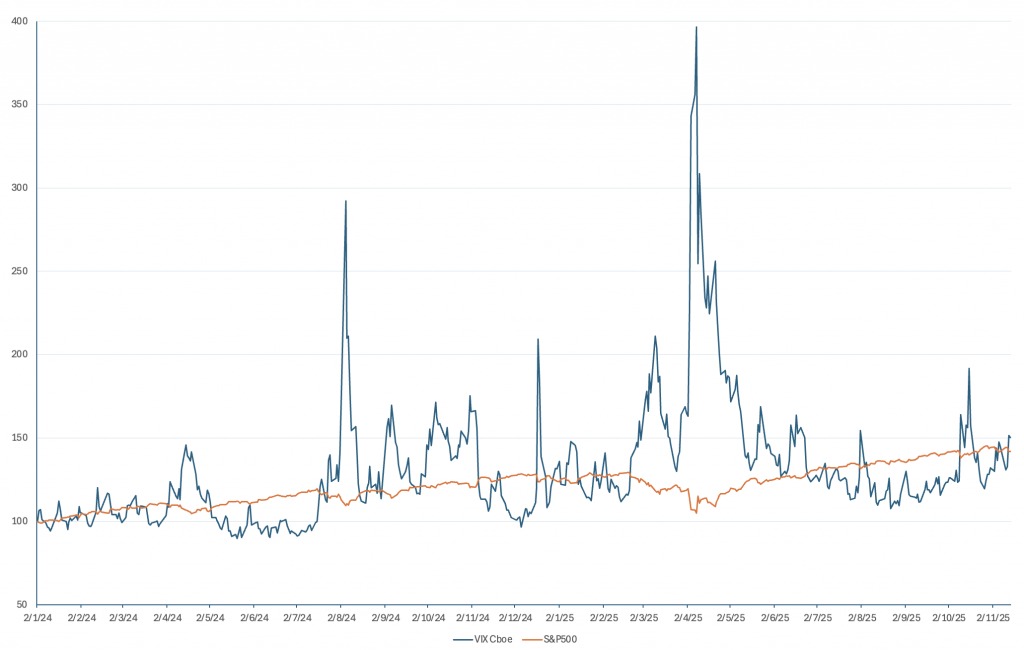

What is the VIX and why does it matter?

The VIX, known as the “fear index,” measures the expected 30-day volatility of the market through S&P 500 options and serves as one of the best gauges of investor sentiment. When the VIX rises, it indicates that investors anticipate more uncertainty and possible declines, while low levels reflect calm or even complacency, which can also increase the risk of corrections. Although it does not predict the direction of the market, it does help to assess the environment in which we are investing and to detect periods of stress.

Below is a chart showing the prices (on a base of 100) of the VIX and the S&P 500 between January 2024 and November 2025.

The chart clearly shows the inverse relationship between the VIX and the S&P 500, with peaks in volatility coinciding with declines in the index. Two episodes stand out in particular: in August 2024, the violent dismantling of the yen carry trade following the Bank of Japan’s rate hikes, which sent the VIX skyrocketing; and in April 2025, “Liberation Day,” triggered by Trump’s announcement of new tariffs, which caused severe market tensions and the biggest spike in volatility during the period. These events show how the VIX captures moments of financial stress that are not immediately apparent in the indices, helping to better interpret the real market context.

That’s it for the summary!

That’s it for the summary of the last two weeks. We hope it has been useful for you to keep up with the latest economic news and better understand what is driving the markets. We will be keeping an eye on how AI, interest rates, and the other issues that have been shaping these intense days evolve.

If you have any suggestions, questions, or news items you would like us to analyze in future editions, please feel free to send them to us.

Thank you for joining us, and let’s continue learning together!

No responses yet